This post may contain affiliate links. If you make a purchase through these links, a commission may be earned at no additional cost to you. We only recommend products and services that have been personally tested and are believed to provide genuine value to our audience.

The Burry stock market reversal thesis is now one of the most urgent warnings in global finance. Michael Burry argues that the U.S. equity market is sitting at the most dangerous intersection of historic overvaluation, mechanical inflow distortions, and structural fragility ever observed. The combination of stretched valuations, weakening structural support, and rising systemic risk creates what he calls a “coiled spring” a market primed for a violent unwinding.

Throughout stock market history, valuations tend to revert to their long-term averages. The longest stretch above this long-term average was 10 years, between 1960 and 1970. However, the current cycle has kept valuations above their historical mean for 34 years.

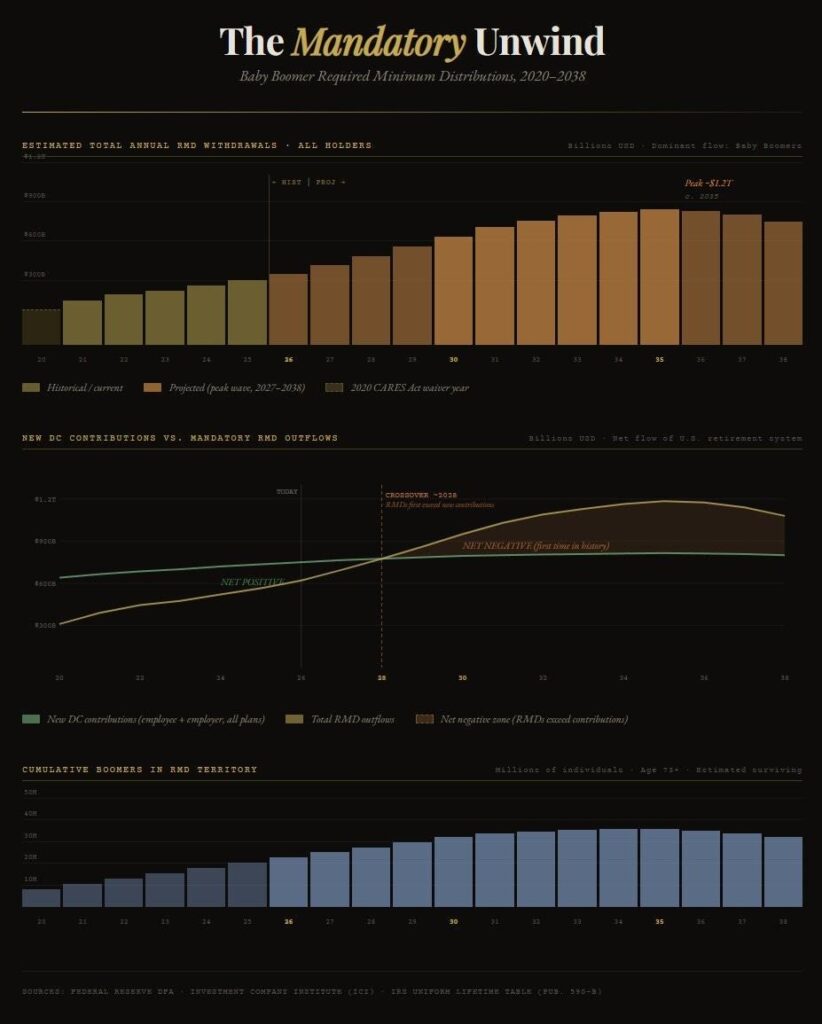

He attributes this to two major structural forces: passive retirement inflows into ETFs and sustained corporate share buybacks. Both of these drivers, however, are now weakening. Corporate buybacks are declining due to heavy AI-related capital expenditures, while the baby-boomer generation has begun to withdraw money from their retirement accounts.

From 2028 onward, retirement funds are expected to experience net outflows an extremely worrying development for equity markets.

1. Burry Stock Market Reversal: Valuations Are at Unprecedented Extremes

- Both the Dow and S&P 500 have spent 34 years above their long-term Shiller CAPE mean more than 10× longer than historical cycles.

- Past secular bears saw the market overshoot to deeply undervalued PEs (5–8x), but the 2008–09 crisis bottomed at merely “fair value,” thanks to massive government support.

- Starting 2026, the Shiller PE is ~40× the second-highest in history.

Downside scenarios based on mean reversion range from −30% to −50%, and −70–80% in extreme troughs similar to 1929, 1974, or 2000.

2. Interest Rates No Longer Anchor Valuation

- Despite a 450 bp jump in yields, the Shiller PE expanded from 28× – 40×.

- This contradicts the Fed Model and demonstrates that market pricing is no longer tied to discounted cash flows.

- With valuation unanchored, pricing becomes a contest between narratives and expectations, which accelerates fragility once narratives crack.

3. The Structural Forces Behind the Burry Stock Market Reversal

Burry identifies four secular drivers that lifted valuations since 1990:

– Passive Investing

- Passive share grew from 6% (1996) – 60%+ (2024).

- Index funds buy indiscriminately, eliminating price discovery and mechanically pushing large caps higher.

- Market-cap weighting creates reflexive loops: higher prices – larger index weights – more inflows – higher prices.

– The Defined Contribution System: A Structural Bid Reversing in the Burry Stock Market Reversal(401k + IRA)

- Auto-contributions created a perpetual bid into equities for decades.

- 2012: DC assets surpassed DB pensions.

- 2028: Redemptions will exceed contributions as baby boomers enter Required Minimum Distributions.

- After 2028, the DC system shifts from a structural bid to a structural ask for the first time in its existence.

– Corporate Buybacks

- From $140B (2000) – $1T+ (2022–2025), overwhelmingly concentrated in mega-cap tech.

- Now collapsing: Q4 2025 buybacks among the largest tech firms fell ~74% YoY.

- Mega-caps are redirecting cash to AI infrastructure + borrowing for capex, not buybacks.

– Policymaker Support That Inflated the Burry Stock Market Reversal Risk

- ZIRP, QE, IOER, TARP, and crisis-era bailouts prevented true valuation resets.

- This created persistent moral hazard and inflated the “permanently high plateau.”

These forces pushed valuations up for decades, but all four are now weakening simultaneously.

Source : Michael Bury

4. Burry Stock Market Reversal: Market Fragility Has Increased Sharply

Ultra-fast, synchronized crashes prove the new fragility

- COVID 2020: Fastest bear market ever; global correlations ~1.0.

- Liberation Day 2025: Simultaneous crash in stocks, bonds, and USD.

The “Shock Index” (loss as % of GDP per capita) was comparable to 1929.

Liquidity is thinner than it appears

- Passive investors don’t sell until forced removing true liquidity.

- HFT provides “phantom liquidity” it evaporates in volatility spikes.

- Pod shops (~$1T AUM) all de-risk simultaneously when models hit stop-loss thresholds.

The market is therefore:

- Less anchored (valuation no longer tied to rates or fundamentals),

- More crowded,

- More momentum-driven,

- More correlated,

- More mechanically fragile.

A small catalyst can create one-way flows through a very narrow exit.

5. The Demographic Cliff: The Most Important Driver of the Burry Stock Market Reversal

- Boomers (62–80 today) hold 30%+ of all U.S. equities.

- RMD withdrawals:

- Now: ~$250B/year

- Early 2030s: >$1T/year

- 2028 is the inflection point when DC redemptions exceed contributions.

This is a permanent structural flow reversal, not a cyclical event.

6. AI Spending Boom: The Wrong Type of Capex at the Wrong Time

- Mega-caps face collapsing free cash flow due to massive AI/data-center capex.

- Alphabet, Meta, Amazon, Oracle are borrowing tens of billions.

- Buybacks are being deprioritized for years.

Burry suggests the market has mispriced the economics of AI infrastructure high capex, low incremental returns, and potential narrative disappointment.

7. The Coiled Spring: Why the Next Downturn May Be Violent

The core of Burry’s thesis:

- Valuations are stretched far beyond historical norms.

- Structural supports (passive flows, DC contributions, buybacks) are fading.

- Liquidity is brittle HFT + pod shops amplify shocks.

- Stock-bond hedge is broken correlations rising toward 1.0.

- AI capex is draining cash from the mega-caps that support the index.

- Demographic selling pressure is imminent and unavoidable.

Therefore:

The next major selloff is likely to be more violent than COVID or Liberation Day and unlike 2020 or 2025, the “Plunge Protection Team” may not be able to reflate valuations quickly.

Expect:

- Deep multiple compression

- Broad cross-asset contagion

- Slow or incomplete recovery

- A narrative-driven unwinding similar to 2000 but potentially larger

8. Bottom Line

Michael Burry believes the U.S. equity market is entering a period where:

- The valuation extreme is unparalleled,

- The structural bid is weakening for the first time in 30–40 years,

- The liquidity profile is fragile and easily overwhelmed,

- The demographic backdrop guarantees future selling, and

- The AI narrative risks becoming the trigger for expectations collapse.

His Conclusion

The multi-decade divergence between U.S. equity prices and underlying fundamentals was created by identifiable, measurable structural forces. Those forces are now reversing. Whether the correction is gradual or sudden, Burry’s analysis suggests its ultimate magnitude, when it arrives, could be historically significant.

Sources: Michael Burry / Scion Asset Management thesis materials. This article is for informational purposes only and does not constitute financial advice.

Where to Build Your Portfolio

You can position your portfolio through the following broker platforms:

REVOLUT:

Easiest option for retail investors. Simple interface, quick access to ETFs, stocks, and commodities.

Trading212:

User-friendly platform offering commission-free stock and ETF investing. Suitable for retail investors seeking straightforward access to global markets.

INTERACTIVE BROKERS: The most professional global trading platform

Most professional global trading platform. Broad asset access, including equities, bonds, futures, commodities, and advanced trading tools.

Frequently Asked Questions

Who is Michael Burry?

Michael Burry is the founder of Scion Asset Management and the investor who famously predicted and profited from the 2008 subprime mortgage collapse. His story was chronicled in Michael Lewis’s book The Big Short and the subsequent 2015 film.

What is the Shiller CAPE ratio?

The Shiller CAPE (Cyclically Adjusted Price-to-Earnings) ratio measures equity valuations relative to 10-year average inflation-adjusted earnings. It is widely used to assess whether markets are over- or undervalued relative to long-term norms.

What are Required Minimum Distributions (RMDs)?

RMDs are mandatory annual withdrawals that the IRS requires from tax-deferred retirement accounts (such as 401(k)s and IRAs) once account holders reach a certain age. As Baby Boomers enter this phase, the retirement system shifts from a net buyer of equities to a net seller.

When does Burry expect the reversal to happen?

Burry’s structural thesis doesn’t specify an exact timeline. However, he identifies 2028 as a critical inflection point, when DC retirement redemptions are projected to exceed contributions for the first time, permanently shifting the retirement system from a structural bid to a structural ask.