Nvidia's $20B Bond Play and the Bitcoin Miners Quietly Betting on AI

Nvidia is going to the debt markets in a big way, and the timing says everything about where the money is flowing right now.

The chipmaker is preparing a multi-part bond offering of at least $20 billion, structured across seven maturities ranging from two to 30 years. The longest-dated bonds are expected to price at roughly 0.9 percentage points above comparable U.S. Treasury securities. Proceeds are earmarked for AI-related investments and refinancing existing debt, signalling a straightforward signal that Nvidia intends to keep building at pace, not wind down.

It's the company's first significant bond offering since 2021, and it comes at a time when demand for AI infrastructure is attracting capital from every direction.

Nvidia's Reach Is Already Global

The bond offering is only part of the picture. Nvidia has been busy cementing its international position, with CEO Jensen Huang's recent visit to South Korea resulting in partnerships with SK Hynix, Naver, SK Telecom, Doosan Group, LG Group, and Hyundai Motor Group. The agreements span memory chips, AI data centers, robotics, mobility systems, and industrial AI, suggesting a wide enough footprint to suggest Nvidia is positioning itself as foundational infrastructure for the next decade of technology development, not just a chip supplier.

For investors tracking where AI spending actually lands, Nvidia's capital allocation decisions carry real weight. As the dominant supplier of GPUs used to train and run large language models, what Nvidia builds and how it finances that building shape the broader AI ecosystem.

Bitcoin Miners See the Same Opportunity

The surge in AI infrastructure spending hasn't gone unnoticed by Bitcoin mining companies. Many of them are sitting on exactly what AI needs: large power capacity, existing data center footprints, and long-term energy agreements. The pivot was almost inevitable.

HIVE Digital, TeraWulf, Hut 8, and CleanSpark have all moved to position themselves as AI and high-performance computing providers alongside their mining operations. The logic is straightforward — by repurposing facilities originally built for Bitcoin mining, these companies can pursue revenue streams that don't rise and fall with crypto market cycles.

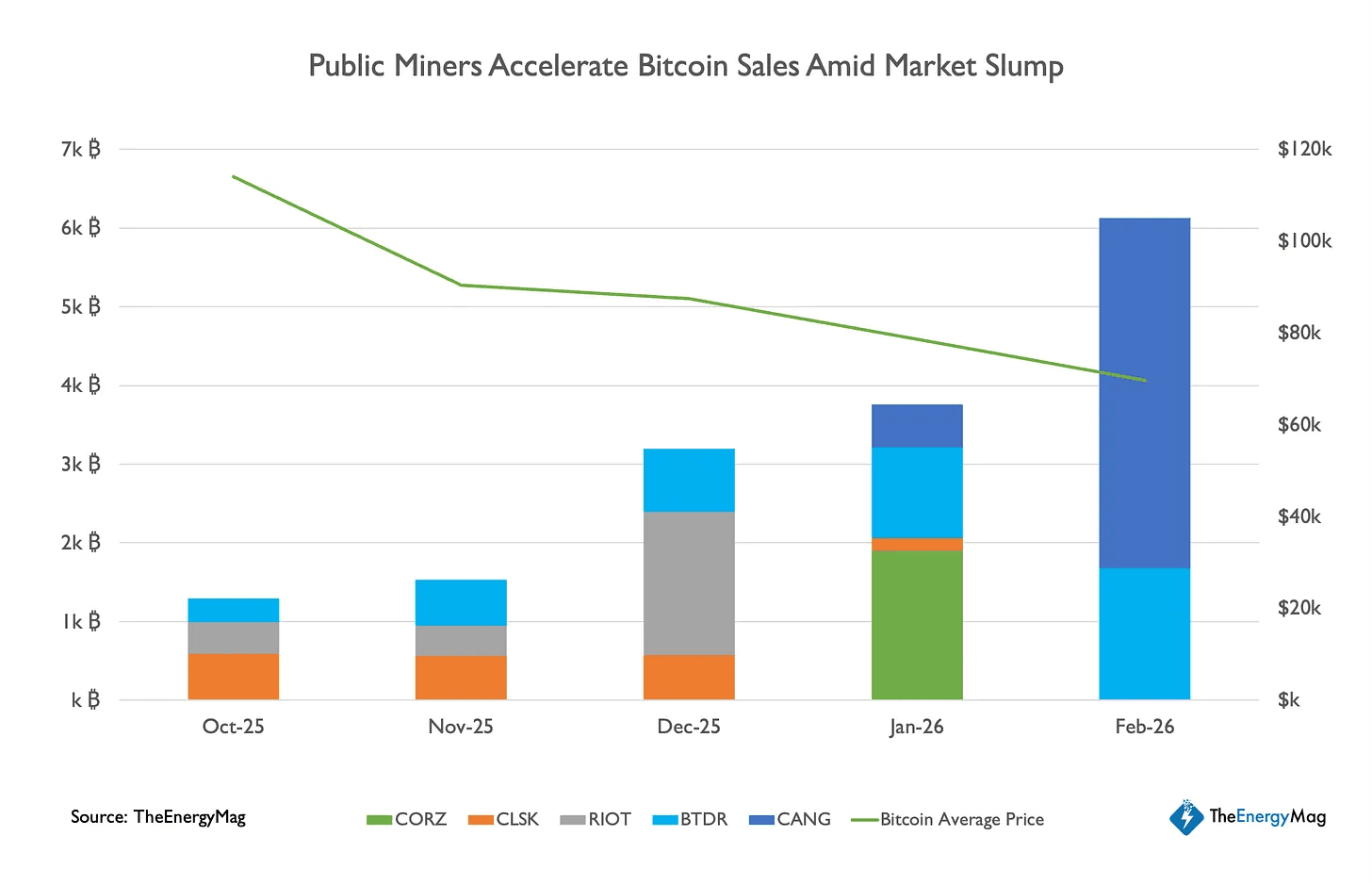

Investors have noticed. While Bitcoin dropped roughly 17% in the opening months of 2026, a basket of Bitcoin mining stocks gained more than 50% over the same period, with the strongest performers up over 70%. Publicly traded miners have collectively announced more than $70 billion in AI and high-performance computing contracts, and some industry projections suggest AI could account for as much as 70% of listed mining company revenue by the end of 2026 up from around 30% today.

The Core Business Is Still Hurting

Strip away the AI headlines, though, and the picture for many miners is considerably less comfortable.

The Bitcoin halving in April 2024 cut block rewards in half, and higher mining difficulty and rising operating costs have been squeezing margins ever since. Some analysts have described the current environment as the toughest the industry has faced in terms of profitability, pushing companies to reduce leverage, sell Bitcoin holdings, and seek income that doesn't depend on the next price rally. Recent market data shows miners sold more than 15,000 BTC between October and March as they adjusted to the new reality.

Canaan's recent numbers put a specific face on those pressures. The Nasdaq-listed miner produced 90 BTC in its latest operational period and received another 24 BTC from customers, showing modest figures that sit alongside a second-quarter revenue guidance range of $35 million to $45 million, well short of analyst expectations of around $96 million. Canaan is also dealing with a second Nasdaq non-compliance notice issued in January after its share price fell below the exchange's $1 minimum bid requirement. The company has until July 13, 2026, to get back above that threshold or face potential delisting proceedings.

Two Trends, One Direction

What connects Nvidia's bond offering and the Bitcoin mining pivot is the same underlying force: AI infrastructure is where the capital wants to go. Nvidia is raising over $20 billion to supply it. Miners are repositioning their existing assets to serve it. The question isn't whether that trend is real, as the money makes that clear enough. The question is which companies are building something durable and which are simply following the capital while their core businesses deteriorate beneath them.